Pricing & Execution: Liquidity, Impact Cost & Slippage

How Mark Price is generated from multi-source oracles — and what that means for your fills.

Introduction

Most traders think about price as a single number — the one flashing on the chart. In reality, every market has at least four prices going at any given moment: the highest someone will pay (Bid), the lowest someone will sell at (Ask), the midpoint between them (Mid), and the platform's reference price for risk and PnL (Mark Price). The gaps between these four numbers are where your trade actually lives.

This guide explains how those prices are constructed, why liquidity determines the size of those gaps, what the impact cost of your order really is, and how slippage shows up when you cross the order book. Once you can see the order book this way, the difference between a good fill and a bad one stops feeling like luck.

1. The Order Book in Plain Language

An order book is just two queues of orders, sorted by price.

- The Bid side is everyone who wants to buy, sorted from highest price down. The top of the bid is the best bid — the highest price any buyer is currently offering.

- The Ask side (sometimes called Offer) is everyone who wants to sell, sorted from lowest price up. The top of the ask is the best ask — the lowest price any seller is currently asking.

The Mid Price is exactly halfway between the two:

Mid Price = (Best Bid + Best Ask) / 2

The gap between them is the spread:

Spread = Best Ask − Best Bid

A tight spread — say, $0.10 on a $50,000 BTC quote — means the market is liquid and competitive. A wide spread — say, $5 on the same quote — usually means thin liquidity, fast-moving conditions, or both. Spread is the cheapest, most visible measure of how expensive it will be to trade right now.

2. Liquidity: Depth Beyond the Top of Book

The best bid and best ask are only the surface. Behind them sit dozens or hundreds more orders at progressively worse prices. This stack — known as market depth — is what actually determines how an order of meaningful size will execute.

A useful intuition: imagine you want to buy $1,000,000 worth of an asset where the best ask shows only $50,000 of size. You will fill the first $50,000 at the best ask, then the next chunk at the second-best ask, and so on, walking up the book until your order is fully filled. Your average fill price will be higher than the best ask you saw when you clicked.

The deeper the order book, the less your order moves the market while filling. A "liquid" market is simply one where you can transact size without moving price much. A "thin" market is one where even a modest order can shift the quote noticeably.

This is also why the same dollar order can have very different execution quality across different times of day, different assets, and different exchanges — not because anyone is treating you differently, but because the depth of the book in front of you genuinely is different.

3. Impact Cost: The Hidden Price Tag of Size

Impact cost is the formal name for how much your order moves the market while it executes. It's the difference between the price you would pay if you could trade an infinitely small amount, and the average price you actually pay given the size you actually traded.

A worked example. Suppose the order book shows:

- Best ask: $50,000 for 0.5 BTC

- Next ask: $50,010 for 1.0 BTC

- Next ask: $50,025 for 2.0 BTC

You want to market-buy 2 BTC. Your fills look like:

- 0.5 BTC at $50,000 = $25,000

- 1.0 BTC at $50,010 = $50,010

- 0.5 BTC at $50,025 = $25,012.50

Total cost: $100,022.50, for an average fill of $50,011.25 per BTC.

If you could have traded "infinitely small" at the top of the book, your reference price would be the best ask, $50,000. The difference — $11.25 per BTC, or about 2.25 basis points — is your impact cost.

Two things to take away:

- Impact cost grows as a function of size relative to depth. Doubling your order size on a thin book often more than doubles your impact cost.

- Impact cost is invisible in the trading fee line. It doesn't show up as a charge — it shows up as a worse average fill price.

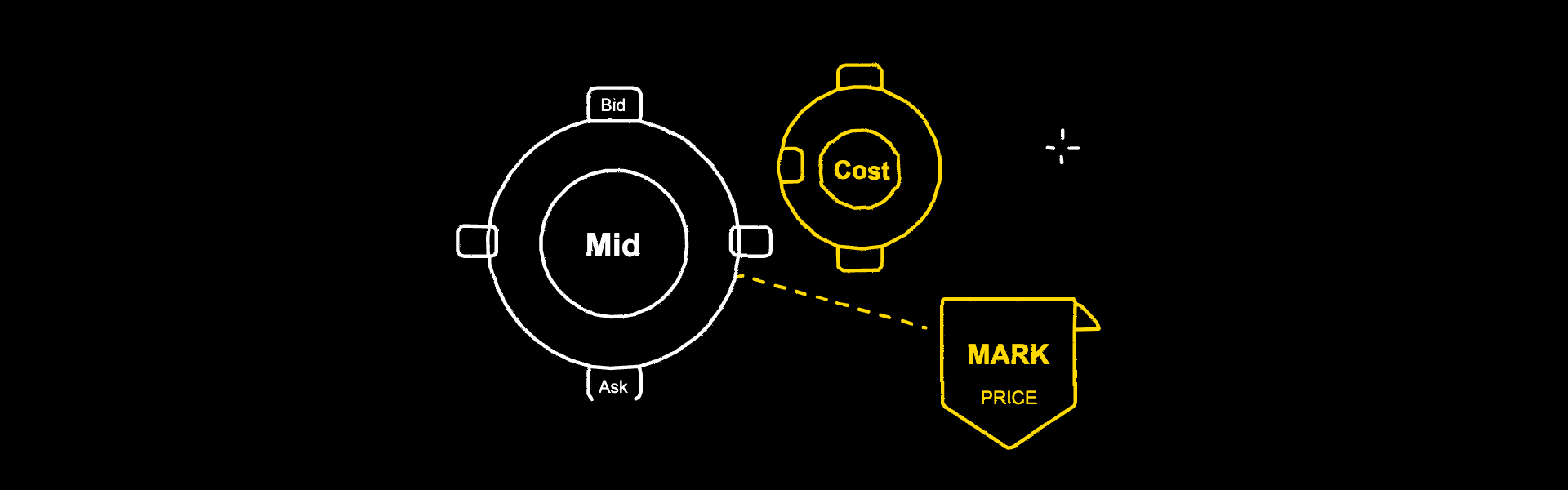

4. Mark Price

The Mark Price is the platform's fair-value reference for your position. It's used to calculate unrealized PnL, to decide when liquidations trigger, and to set funding rates on perpetuals. It is not simply the last trade price — last price can be moved by a single large taker, or by manipulation on a thinly traded venue, neither of which reflects "fair value."

How MC Markets generates Mark Price:

Mark Price = Weighted aggregate of multi-source external oracle prices and internal platform data

The platform references spot prices from multiple oracles — including Chainlink and Pyth — and combines them with internal data to produce a “Fair Aggregated Price.” Multi-source aggregation makes Mark Price resistant to anomalies or manipulation on any single data source — preventing unjust liquidations triggered by a single outlier price.

Oracle Price: References from Chainlink and Pyth oracles for spot benchmarks.

The practical implication: when the market is calm and deep, Mark Price stays very close to Mid. When the market is volatile or one side of the book is depleted, Mark Price diverges from the headline last-trade price in ways that protect you — your liquidation price, for example, isn't decided by a single rogue trade on the order book.

5. Slippage: The Final Piece

Slippage is the difference between the price you expected and the price you got. It comes from two sources:

- The price moved between your decision and your fill. Markets don't pause while you click — the ask you saw a second ago might be gone by the time your order hits the matching engine.

- Your order walked the book. As covered above, any market order larger than the best-level size pays progressively worse prices on each level.

Most platforms — including this one — give you a slippage tolerance setting. If the actual fill would deviate from the expected price by more than your tolerance, the order is rejected instead of filled.

Default tolerances on this platform are:

- 8% for spot orders

- 10% for derivatives orders

You can tighten these in your order settings. Tighter = stronger protection but a higher chance of rejection in fast-moving markets. Looser = more reliable fills but more exposure to bad prints. The right setting depends on the asset's normal volatility and whether you'd rather miss a trade than fill it badly.

6. How to Trade With the Mechanism, Not Against It

Five practical habits, ordered by impact:

- Use limit orders for size. Instead of crossing the spread with a market order — which guarantees you pay the full impact cost — place a limit at or near the mid. You give up some certainty of execution in exchange for a much better average price.

- Check depth before clicking. Most platforms show order book depth or a market-impact estimate. For a non-trivial order, glance at the next several levels — not just the best bid/ask — before committing.

- Break large orders into smaller pieces. Rather than market-buying 50 BTC at once, trade in chunks over time. Algos do this automatically (TWAP, VWAP); manually you can do a simpler version with the same intent.

- Avoid trading the open and close. Spreads tend to widen and depth thins out around session open/close and around major news. Trading 30–60 seconds after a print rather than at the print itself often saves real money.

- Calibrate your slippage tolerance. Defaults are conservative for safety, but on a calm day, tightening the tolerance for large spot orders prevents you from filling at runaway prices in a momentary spike.

The principle behind all five is the same: the order book is a mechanism, not an opponent. Once you trade with awareness of how it actually works, you stop paying the "tax" most retail flow pays without realizing it.

Quote Formula: Buy: QuoteAsk = MarkAsk + ImpactPrice(N); Sell: QuoteBid = MarkBid - ImpactPrice(N). Impact cost increases with order size. The platform provides an estimated impact cost before you confirm your order.

7. Quick Recap

The four ideas worth taking with you:

- Mid Price = (Best Bid + Best Ask) / 2. The spread between bid and ask is the most visible measure of liquidity.

- Impact Cost is the price movement your own order causes while filling. It grows non-linearly with size relative to depth and never appears as a fee — it just shows up as a worse average price.

- Mark Price is generated from a weighted aggregate of multi-source oracle prices and internal platform data — it is the platform's fair-value reference price, and the sole basis for PnL calculation and liquidation. It is designed to be resistant to single-trade price manipulation.

- Slippage combines time-based price movement and order-walking the book. Slippage tolerance settings (default 8% spot, 10% derivatives) protect you from extreme outcomes; tighten them deliberately on calm days, leave them looser when speed matters.

Risk Disclosure

The pricing and execution mechanisms described here represent the platform's standard methodology and may be updated from time to time; always check the official documentation for the current parameters. Trading involves substantial risk and can result in losses exceeding your initial deposit. Past performance does not guarantee future results. Trade only with capital you can afford to lose.